Have your life circumstances changed since you took out your life insurance policy? Policyowners sometimes find themselves wondering what happens when they surrender a life insurance policy or whether it still makes sense to keep paying for one. That’s perfectly normal. The reason you bought life insurance may no longer apply — perhaps your children are grown and financially independent, your original beneficiary has since passed, or premiums have simply become too expensive. No matter your situation, surrendering a life insurance policy is one way to end coverage and access the value you’ve built over the years.

Surrendering a life insurance policy involves terminating your coverage in exchange for a cash payout. When you surrender your policy back to the insurance company, you’ll receive its cash surrender value — the amount that has accumulated within the policy, minus any applicable fees, outstanding loans, or interest owed.

If you’re considering surrendering your policy, let’s explore the common reasons people choose to do so, what the process looks like, and alternatives that may be more financially rewarding than surrendering your life insurance policy outright.

Key Takeaways

- Surrendering a life insurance policy means ending your coverage in exchange for a cash payout from your insurer, known as the cash surrender value.

- The cash surrender value is typically your policy’s accumulated cash value minus any fees, loans, or unpaid premiums.

- Once surrendered, your policy is permanently terminated, and your beneficiaries will no longer receive a death benefit.

- You may face surrender charges or tax implications—any gains above the total premiums you’ve paid (your tax basis) may be taxable as ordinary income or capital gains.

- Reasons to surrender often include reduced financial need, unaffordable premiums, or the need for immediate cash.

- Before surrendering, consider alternatives such as reducing coverage, using your policy’s cash value to pay premiums, or selling your policy through a life settlement for a potentially higher payout.

- Coventry Direct can help determine if your policy qualifies for a life settlement, allowing you to unlock greater value than surrendering it to your insurer.

What Does It Mean to Surrender Your Life Insurance Policy?

Surrendering a life insurance policy means voluntarily canceling permanent coverage in exchange for its accumulated cash value, paid to you by your insurer. In practical terms, you are returning the policy to the insurance company and, in return, receiving the cash surrender value: the money that has built up inside the policy over time, minus any surrender fees, outstanding loans, or unpaid premiums. Once the surrender is complete, the coverage ends, and there is no death benefit for your beneficiaries.

This option is typically available only for permanent life insurance policies such as whole life or universal life, since they include a savings or investment component. Term life insurance policies don’t accumulate cash value, so surrendering them usually means ending coverage without receiving any payment.

For many policyowners, surrendering a life insurance policy can be a way to access immediate funds or reduce financial strain from ongoing premium payments. However, because surrendering permanently ends your coverage and may result in less money than other options, it’s worth exploring alternatives such as a life settlement, which can often provide significantly more value for qualifying policies.

Why You Might Not Want to Surrender Your Life Insurance Policy

While surrendering a life insurance policy can provide short-term financial relief, it’s not always the best long-term decision. There are several potential drawbacks to consider before moving forward:

- Loss of coverage and benefits: Once you surrender, your life insurance policy ends permanently. Your beneficiaries will no longer receive a death benefit, and reinstating coverage later can be difficult or costly—especially if your health has changed.

- Possible surrender charges: Most permanent policies include surrender fees, particularly in the early years. These fees can significantly reduce the payout you receive

- Tax consequences: Any amount you receive above your total paid premiums (your tax basis) may be taxable as ordinary income or, in some cases, capital gains. This can reduce the overall value of your surrender payout.

- Lower return compared to a life settlement: For qualifying policyowners, selling your life insurance policy through a life settlement can yield substantially more money, on average, several times greater than the cash surrender value. This makes surrendering less appealing for those who qualify.

- Reduced estate or legacy value: If you originally purchased your policy for estate planning or wealth transfer purposes, surrendering could eliminate a key financial safeguard for loved ones or beneficiaries.

Before deciding to surrender your policy, it’s wise to compare your options carefully. For many, exploring a life settlement provides a more financially rewarding alternative that allows you to unlock the value of your policy while eliminating future premium obligations.

What happens when you surrender a life insurance policy?

When you decide to surrender your life insurance policy, you’re choosing to end your coverage in exchange for a cash payout from your insurer. The process is straightforward but final—once completed, your policy is permanently terminated, and your beneficiaries will no longer receive a death benefit.

Let’s walk through the steps it takes to surrender your policy and what happens when you do.

When you surrender your life insurance policy for the cash surrender value, you are essentially canceling your life insurance coverage. After you receive the cash surrender value — minus any surrender fees owed to the life insurance provider — your life insurance coverage ends. When you die, your beneficiaries will not receive the death benefit.

The process of surrendering your policy is relatively easy:

- Contact your insurance company. You can initiate the surrender process over the phone. The insurance agent will walk you through the steps and documentation required to collect any cash surrender value you may have. They can also inform you about any fees you’ll be charged.

- Submit documentation. You’ll likely need to supply a surrender request form to your life insurance provider.

- Receive cash surrender value. After the life insurance provider has processed your request, you can expect to receive the cash surrender value funds via check or electronic transfer.

- Obtain policy termination confirmation. Upon receiving the cash surrender value, expect to receive a confirmation of policy termination by mail from your life insurance provider. If they do not provide this, you can request that you receive confirmation of policy termination.

Once the policy is surrendered and the payout is received, your coverage ends permanently — meaning your beneficiaries will no longer receive a death benefit. Before finalizing the surrender, it’s worth reviewing your options to ensure you’re getting the most value possible from your policy. In some cases, selling your policy through a life settlement may provide a much higher return than surrendering it to your insurer.

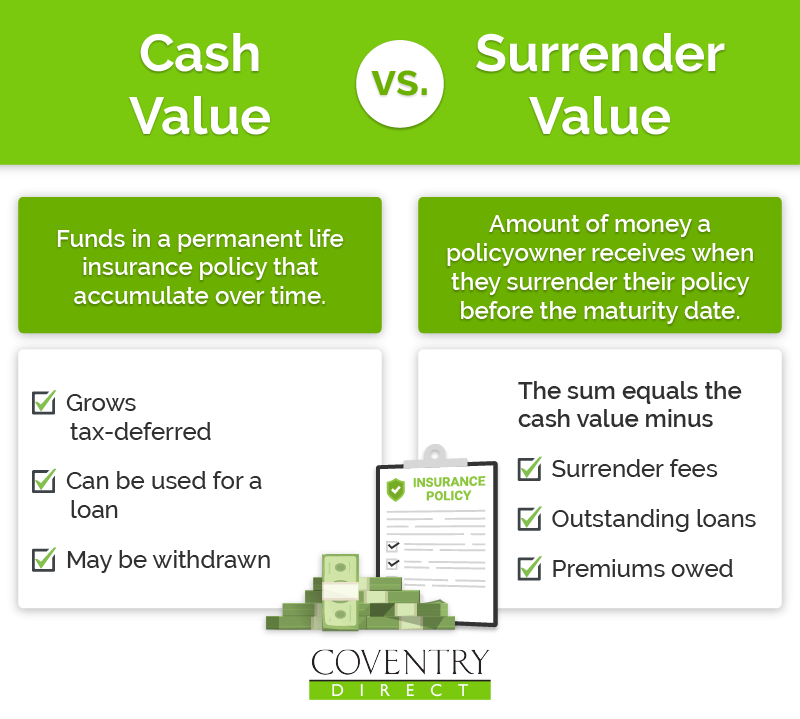

What is cash surrender value?

Cash surrender value is the amount of money that accrues within certain policy types and is returned to the policyowner when they surrender a life insurance policy. The cash surrender value typically totals the cash value minus any fees, loans, or outstanding premiums owed.

Cash surrender value vs cash value?

While many assume the surrender value means the same thing as cash value when talking about life insurance, they’re actually two different things.

Cash value is the amount of money that accumulates over time in a permanent life insurance policy. It grows tax-deferred and can be accessed via loan or withdrawal.

Surrender value, however, is the amount of money that will actually be returned to you upon surrendering the policy. This payout amount includes the cash value minus any fees, loans, or premiums owed.

When it comes to surrendering vs. cashing out a life insurance policy, the key difference lies in what happens to your coverage. Cashing out usually refers to accessing your policy’s cash value while keeping the policy active, often through a partial withdrawal or loan. Surrendering, on the other hand, means permanently ending your coverage in exchange for the full cash surrender value. If you still want some protection in place—or want to avoid surrender fees—cashing out part of your policy may be a more flexible option than surrendering it entirely.

Common reasons why people surrender their life insurance policy

Surrendering a policy happens because life can be unpredictable. While most folks who take out a permanent life insurance policy — such as a whole life insurance policy or a universal life insurance policy — plan on keeping it until the end of life so their beneficiaries can collect the death benefit, sometimes circumstances arise that require a course correction. Here are some of the most common reasons people choose to surrender their life insurance policy:

- Adult children are no longer financially dependent: If a policyowner took out a policy to protect their young children, they may find that 20+ years later, their adult children no longer need the financial support upon the insured’s death.

- Their spouse has passed: Another common reason someone may surrender their policy is that their spouse has died. Typically, the breadwinner of the family may take out a life insurance policy to protect their spouse. However, if the spouse passes before the family’s breadwinner does, the policy may be unnecessary.

- Finances are tight: When a policyowner experiences decreased financial stability, they may consider surrendering their life insurance policy. If they find it challenging to pay premiums, they may give up the policy altogether and collect any cash surrender value that may have accrued.

- Better investment opportunities: For folks who use their life insurance policy as an investment vehicle, they may find that the returns of their policy’s cash value are not as favorable as an alternative investment opportunity. Instead of keeping their cash in an account with limited growth potential, they may take the cash surrender value and redirect it into investments they believe will yield higher returns.

- They need cash now: Sometimes unexpected expenses show up — healthcare bills, retirement living expenses, and long-term care costs for example. Policyowners may want to surrender their policy to pay for these unexpected financial obligations rather than wait for the death benefit to pay out to their beneficiaries later.

What are the consequences of surrendering a life insurance policy?

There are a few consequences of surrendering your life insurance policy. First, you’ll no longer have life insurance coverage. If you die, your beneficiaries will no longer receive the death benefit from your life insurance since the policy is no longer in effect. Second, surrendering the policy can come at a financial loss. The cash surrender value is often lower than the total premiums paid, so you’re not extracting as much value from the policy as you paid into it. Plus, you may be responsible for paying surrender fees. Finally, you may find yourself with a tax bill if you have an outstanding loan from the policy. It’s better to pay off any debts owed to the policy before surrendering it.

Will surrendering my life insurance policy have any tax implications?

Yes, surrendering your life insurance policy could result in a tax bill. The total amount you’ve paid in premiums over the life of the policy is called your tax basis, and that portion is not taxable. However, any amount you receive above your tax basis may be subject to taxation.

Here’s an example: Imagine you’ve paid $12,000 in total premiums on your life insurance policy. When you surrender it, your insurer provides a cash surrender value of $18,000.

- The first $12,000 (your tax basis) is tax-free.

- The remaining $6,000 is considered a gain and is generally taxed as ordinary income.

In some cases, if your payout exceeds the insurer’s assigned cash value, that excess portion could be taxed as a capital gain rather than ordinary income.

In summary:

- Premiums you’ve paid: Tax-free return of principal

- Gain up to the policy’s cash value: Typically taxed as ordinary income

- Amount above the insurer’s cash value: May be taxed as capital gains

Because each situation is unique, we recommend speaking with a tax or financial advisor before surrendering your policy. They can help you understand your specific tax exposure and explore whether selling your policy through a life settlement might yield a higher after-tax value than surrendering it outright.

An alternative to surrendering your policy: sell it for cash

If you’re looking for a way to receive more money from your life insurance policy than surrendering it would offer, you may want to consider selling it in a life settlement. A life settlement pays, on average, four times the cash surrender value. Here’s how a life settlement works: you sell your policy to a third-party buyer, typically a licensed life settlement provider. They pay you a lump-sum for your policy, take over ownership and premium payments, and receive the death benefit.

There are a few things to consider if you decide to explore a life settlement:

- There’s a qualification process. Folks who have a policy that’s worth $100,000 or more may qualify to sell their life insurance policy.

- You can sell all — or some — of your policy. Some policyowners want to sell their entire policy while others want to retain a portion of the death benefit for their beneficiaries (also known as a retained death benefit). This option enables you to sell a portion of your policy while retaining some coverage with no future premium obligations.

- Terminally ill folks may qualify for a viatical settlement. Insured’s with a terminal or chronic illness can qualify for a viatical settlement instead of a life settlement. Viatical settlements tend to have a higher payout and can be used toward medical care and living expenses. They’re also generally tax-advantaged.

If you’re interested in exploring a viatical or life settlement, contact Coventry Direct to find out how much your policy may be worth.

Know your options with Coventry Direct

No matter what you decide to do with your life insurance policy, remember that your policy is exactly that: YOUR policy. It’s an asset you own and one that you’ve paid into for years. If it’s no longer serving you the way you want, it may be time to adjust your life insurance strategy by surrendering or selling your policy. Reach out to the experts at Coventry Direct to learn more about your options. Coventry can evaluate your policy to determine if it qualifies, giving you one more piece of information to consider before making a decision about what to do with your life insurance policy. Contact us today to learn more and get started.

Common Questions about Surrendering a Life Insurance Policy

Surrendering a life insurance policy can raise a lot of questions—especially around what you’ll receive, what fees or taxes may apply, and how the process works. Whether you’re considering surrendering life insurance policy coverage for financial reasons or simply no longer need it, understanding the basics can help you make a more informed decision. In the following sections, we’ll cover the most common concerns, from potential cash value payouts to tax implications.

What are surrender fees?

Surrender fees are charges that insurers deduct when a policyholder chooses to cancel their life insurance policy early. These fees can significantly reduce the cash surrender value a person receives from the policy.

What is a surrender period?

The surrender period is the initial number of years during which canceling a policy results in surrender charges. This period varies by insurer and policy type but typically lasts between 5 to 10 years.

Surrendering in a Term Life Insurance vs. Permanent Life Insurance policy, what’s the difference?

Term life insurance provides coverage for a set number of years and does not accumulate any cash value, meaning there’s nothing to collect if you surrender (i.e. cancel) it. Permanent life insurance, however, features higher premiums, includes a cash value component, and comes in types like whole life, universal life, and variable life insurance. When you surrender a permanent life insurance policy, there may be surrender value you can receive from it.

What is a lump sum payment for the value of a life insurance policy?

When surrendering life insurance policy coverage, policyholders may receive a lump sum payment equal to the remaining cash value, after fees. This is typically a one-time payout instead of structured installments.

What does it mean to surrender a life insurance policy?

To surrender a life insurance policy means to end your coverage in exchange for a cash payout from your insurer. When you surrender the policy, the insurance company pays you the cash surrender value—the amount that has built up inside your policy, minus any fees, loans, or outstanding premiums. Once surrendered, the policy is permanently terminated.

What happens when you surrender a life insurance policy?

When you surrender your life insurance policy, your insurer processes the cancellation and sends you the cash surrender value. You’ll stop paying premiums, and your beneficiaries will no longer receive a death benefit. It’s important to know that surrendering is final, and you may owe taxes on any gains above what you’ve paid in premiums.